Five Reasons to Buy a Fixed Index Annuity

Reason #1: It’s a strategy designed to help survive a bear market

While no one can predict the next bear market most investors today understand there are different cycles of the business of expansion and contraction and there are different cycles in the stock markets, bull and bear markets. For example from 1981 to 1999 we had what was called a secular bull market, and if you were an investor back in 2000 you know, it ended very badly. We went into a bear market, and the market dropped about 50%. And in the next 3 or 4 years after that we had a bull market and then during the crash of 2008 the market dropped 57%.

Now here’s the good news: we’ve been in a 10-year bull market since 2009. And nobody knows when exactly the next bear market is. So this might be a good time to consider having a strategy designed to help survive a bear market.

It might be time to take some money off the table. One strategy to do this it remove part of your portfolio into something that is designed to help survive the bear market. An option available to you is to take a percentage of your assets that may be at risk in equities and purchase a fixed indexed annuity. If you are going to purchase an insurance contract that gives you guarantees, you may have upside potential normally with limits, but you’ll have downside protection. That means that you’ll have limited participation on the market indexes going up, but if the market drops 50%, you have a strategy that help protect from the downside.

REASON #2: Participate in limited upside market performance.

Most retired investors have diversified portfolios that have traditionally been proportioned between bonds, CDs, Treasury, and equities. If you’ve been in equities the last ten years, I don’t know how you couldn’t be doing well. But perhaps you look at the other part of your portfolio that’s more in conservative, yielding type of investments and see your returns have been very minimal, maybe 1 or 2%.

Economist Roger Ibbotson published a White Paper in 1979 that revolutionized the financial planning industry. What he did was produce was a 90-year chart that showed the difference in returns between stocks, bonds, and Treasuries. And in this report, the equities normally outperformed bonds 2:1. Just recently in March of this year, he came out with another study. He used the same methodology to compare fixed indexed annuities with bonds, CD’s, and Treasuries. He went back and used historical data, and his findings were just this, stocks still outperformed bonds 2:1 (now I would tell you in the last ten years it’s probably more like 3:1 because as you know interest rates have been so low and equities have done so well). So, he added FIA’s as an asset class, and this was his findings: equities outperformed bonds, but fixed index annuities as an asset class outperformed bonds too. From my own experience, I’ve seen fixed index annuities do somewhere between 4-5%. I think I’ve seen Treasuries and CDs closer to 1.5-2.5% in the last ten years.

https://dta0yqvfnusiq.cloudfront.net/commo93759149/2018/02/Ibbotson-White-

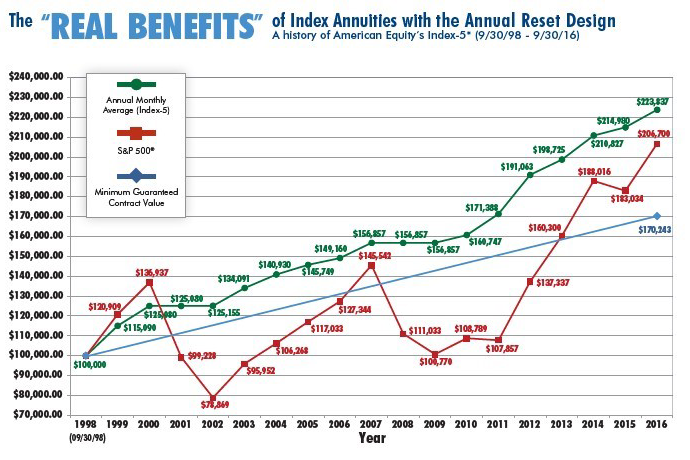

Look at the performance of this American Equity FIA in the last 20 Years. As you can see from this illustration from American Equity, a life insurance selling annuities, it shows the performance since 1998. Now as we talked about before, the performance also includes two bad bear markets. The bear markets are just part of the process. It’s like breathing in, breathing out. You can see in this illustration what happened. So in the good years for the market, the market outperformed the fixed index annuity, but the reason why the annuity performed well is that it did not experience any 50% draw down.

https://media.american-equity.com/Documents/8109-10.21.16.pdf

REASON #3: Annuities have no memory – you keep what you kill

You know all investors are certainly excited after having a great ten years. They’re looking at their statements after ten years and saying, boy I’m a lucky person. But did you realize in equities there’s no lock down in there?

I have always been a fan of the actor Vin Diesel. I think one of the best movies I have seen that he starred in was called Riddick. He was fighting this whole empire called the Necromongers. The whole theme of it all was that you took what you wanted by force, and you kept what you killed. Basically, if you took over a planet, it was yours. And you’re saying, John, what does this have to do with fixed asset annuities?

Well, what annuities allow you to do since they have no memory, at the end of every anniversary your return is locked in. In equity portfolios, your return is not locked in so if the market goes down not only does your original amount go down but your accumulated returns go down. For example, you made 6% one year and 10% the next year, and then the market drops 50%, the whole value drops 50%. Now, if we take that same example with an indexed equity annuity and you made 6% one year and 5% the next year and then the market drops 50%. Well, the principal plus the annual returns are locked in, and you get to keep what you’ve earned. But remember, annuities have a cap on the positive returns so you will miss a part of the gain on the way up. In very good markets, especially when the returns are close if not exceeding 10%, your returns will be muted in the annuity.

REASON #4: Tax Deferral.

Possibly there’s a 15-25% benefit depending on your tax bracket. It’s only a benefit if it’s unqualified money. So, you do get tax deferral benefit by purchasing an annuity. It may be a big thing for some people I mean the way I look at it, it doesn’t cost any more and if you’re having a little bit of a tax problem, who doesn’t want to pay fewer taxes today. But you or your beneficiaries are going to have to pay.

REASON #5: Lifetime Income

This product has the potential to give guaranteed income for the rest of your life. Now when I first started working in the business in the 1980s most retirees had what we call the three legs of their investments: they had Social Security coming in, they had pensions coming in, and they took some money out of their savings or investments. So the big majority of their income came with guarantees. Fast forward to today, very few people out there have a pension. So the only guaranteed income they have coming in is maybe from Social Security. Sometimes people just want to have a base of income. There’s a couple of ways of turning annuities into guaranteed income for life. One way is to annuitize (which I would probably not recommend) and the second way is to purchase one of these riders that gives you a guaranteed income value benefit that goes up every year if you don’t use and then it guarantees income for life. In some cases, this gives the retired investor a base, so perhaps they can be a better investor with their other money-sometimes not. It may not be worth the expense especially if you don’t use the income rider. It normally costs about 1% annually. It is important to remember all guarantees are back by the claims paying ability of the insurer.

The income riders are also fairly complicated and sophisticated, so I went ahead and did a video focusing on that. (Click HERE to watch Building Your Guaranteed Income Floor VIDEO).

Is your current annuity not performing? You know, the market has been giving double-digit returns for years. However, you aren’t seeing it. Are you confused about your income options? Do you have an income rider that you don’t understand? Are you an annuity orphan? Well, maybe I can help. I certainly would be glad to. You don’t even have to come to the office, just shoot me an email or give me a phone call. I will either contact you directly or respond to your email. If you want to set up a time to talk to me on the phone, give my office a call.

Sincerely,

John Romano CFP®

Sincerely, John Romano CFP®

John Romano, CERTIFIED FINANCIAL PLANNER™, has over 30 years experience in the financial field. John is a Registered Representative with Securities America, Inc. (member of the FINRA and SIPC), and an Investment Advisor Representative with Securities America Advisors. He has prepared hundreds of reports for retirees to assist in their retirement income planning needs. He is dedicated to providing portfolio analysis, dividend and income information, and investment management services to retirees (and those preparing to retire) in The Villages, Florida, and throughout the United States.

Securities offered through Securities America, Inc. Member FINRA/SIPC, John Romano CFP® Registered Representative. Advisory Services offered through Securities America Advisors, Inc. John Romano Investment Advisor Representative. Romano Income Strategies and Securities America are not affiliated.

Trading instructions sent via e-mail may not be honored. Please contact my office at (352)753-8590 or Securities America, Inc. at (800) 747-6111 for all buy/sell orders. Please be advised that communications regarding trades in your account are for informational purposes only. You should continue to rely on confirmations and statements received from the custodian(s) of your assets. The text of this communication is confidential and use by any person who is not the intended recipient is prohibited. Any person who receives this communication in error is requested to immediately destroy the text of this communication without copying or further dissemination. Your cooperation is appreciated.

John Romano, CFP®

305 Skyline Drive, Suite 3, Lady Lake, FL 32159

Phone: 352-753-8590

Email: John@RomanoJohn.com

The opinions and forecasts expressed are those of the author, and may not actually come to pass. This information is subject to change at any time, based on market and other conditions and should not be construed as a recommendation of any specific security or investment plan. Past performance does not guarantee future results. Fixed index annuities are intended for retirement or other long-term needs. It is intended for a person who has sufficient cash or other liquid assets for living expenses and other unexpected emergencies, such as medical expenses. Fixed Index Annuities are insurance contracts and should be considered complex products. Fixed Index Annuities are not stock market investments. You are never invested in the index itself. Fixed index annuities are subject to possible surrender charges and a 10% IRA early withdrawal penalty prior to age 50 Y. Early withdrawal charges and Market Value Adjustments (MVA) may apply. Withdrawals may reduce any optional guaranteed amounts in an amount more than the amount of the withdrawal. Taxable distributions are subject to ordinary income taxes.

Current minimum return, principal value and prior earnings guarantees by the issuing insurance company, subject to their claims paying ability, and contract provisions.

Indexed interest is calculated and credited (if applicable) at the end of an annual interest term based on the strategy selected and will be adjusted for any caps, spreads, performance triggers or participation rates, all which can limit or reduce the interest credited. Outcomes may differ based upon the interest crediting strategy selected and assume compliance with the product's benefit rules. Not all strategies are available in all states and firms. Amounts withdrawn from the indexed account before the end of an interest term will not receive indexed interest for that term. Interest credited to the indexed accounts is affected by the value of outside indexes and the annuity will not experience returns identical to the index's performance. Values based on the performance of any index are not guaranteed. The contract does not directly participate in any outside investment..

Indexed interest caps, fixed account interest rates and margin rates may be reset at the end of each interest term. Interest Rates, indexed interest caps and margin rates are subject to change without notice.

Tax qualified contracts such as IRAs, 401(k)s, etc. are tax deferred regardless of whether or not they are funded with an annuity. If you are considering funding a tax-qualified retirement plan with an annuity, you should know that an annuity does not provide any additional tax-deferred treatment of earnings beyond the tax-qualified plan or program itself. However, annuities do provide other features and benefits such as death benefits and income payment options.

Annuity contracts have terms and limitations for keeping them in force. Although Fixed Index Annuities guarantee no loss of premium due to market downturns, deductions from your Accumulation Value for additional optional benefit riders could under certain scenarios exceed interest credited to your Accumulation Value, which would result in loss of premium. They may not be appropriate for all. Please contact your financial professional or insurance producer for complete details.